Gas & Power: Energy markets looking for a direction after the Easter break

Gas & Power Podcast #38 In this week’s podcast, Julien Hoarau discusses the recent decline in global coal prices due to weak demand and the…

European gas prices were mixed on Friday as concerns on Russian deliveries were offset but ongoing strong LNG supply and weaker demand. The additional drop in coal prices (-3.49% for API2 1st nearby prices, -1.11% for Cal 2023 prices) exerted downward pressure. On the pipeline supply side, Russian flows were almost stable on Friday, averaging 223 mm cm/day, compared to 222 mm cm/day on Thursday. On their side, Norwegian flows increased slightly, to 304 mm cm/day on average, compared to 300 mm cm/day on Thursday.

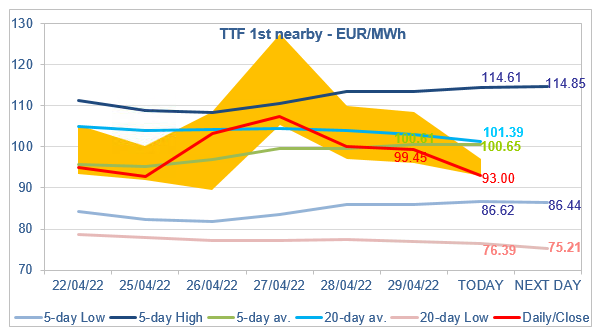

At the close, NBP ICE June 2022 prices increased by 3.770 p/th day-on-day (+2.36%), to 163.680 p/th. TTF ICE June 2022 prices were down by 39 euro cents (-0.39%), closing at €99.450/MWh. On the far curve, TTF ICE Cal 2023 prices were down by 76 euro cents (-0.96%), closing at €78.482/MWh.

In Asia, JKM spot prices dropped by 1.76%, to €69.875/MWh; June 2022 prices dropped by 1.61%, to €79.404/MWh.

TTF ICE June 2022 prices resisted the downward pressure and managed to close around the 5-day average on Friday. They are down this morning, to 93.00/MWh at the time of writing. Yes, concerns on Russian deliveries remain a supporting factor but, given the level of Asia JKM prices and the level of the maximum coal switching level (88.47/MWh on Friday), we believe prices have more downside potential than upside in the very short term.