Lost hydrocarbon in the US reaches 1.1 mb/d

Brent prompt future contract slipped back to 67.3 $/b as the lost US production was estimated to be at 1.1 mb/d for last week. The picture…

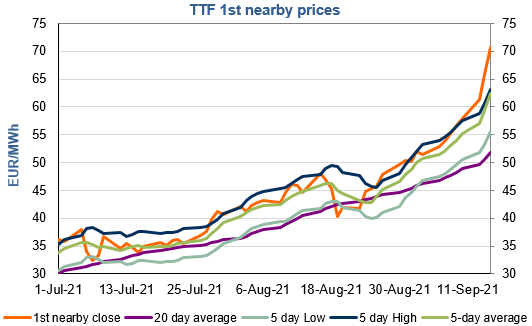

In a very volatile session, European gas prices posted further strong gains yesterday. Concerns that Nord Stream 2 would probably not start commercial deliveries until 2022 continued to lend support. A fire that hit UK’s National Grid’s 2GW IFA power interconnector between France and the UK provided additional support.

The rise in Asia JKM prices (+7.35% on the spot, to €70.757/MWh) (while parity prices with coal for power generation were almost stable) did not help calm the upward pressure.

On the spot pipeline supply side, Russian flows increased again yesterday, averaging 318 mm cm/day (compared to 312 mm cm/day on Tuesday), above the levels of end August (313 mm cm/day). Norwegian flows rebounded, to 280 mm cm/day on average (compared to 242 mm cm/day on Tuesday), as planned maintenance works ended.

At the close, NBP ICE October 2021 prices increased by 12.350 p/th day-on-day (+7.49%), to 177.300 p/th. TTF ICE October 2021 prices were up by 494 euro cents (+7.52%) at the close, to €70.707/MWh. On the far curve, TTF Cal 2022 prices were up by 164 euro cents (+4.05%), closing at €42.066/MWh, increasing the spread against the coal parity price (€35.235/MWh).

European prices are correcting downwards this morning. However, given the concerns on the fundamental situation, the drop should be limited, particularly as prices could benefit from technical supports (€61.801/MWh on TTF October 2021 and €39.135/MWh on TTF Cal 2022).