Bulls keep control of EU gas markets

European gas prices continued to strengthen on Wednesday, supported by cold, dry and not really windy weather forecasts for next week. Dwindling gas stocks and…

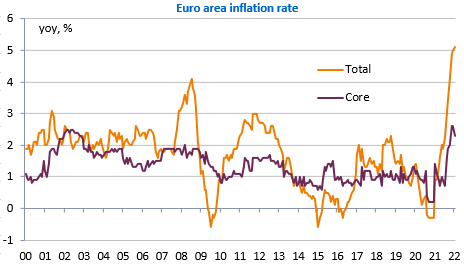

Eurozone inflation finally reached a new high in January (5.1%), driven by energy and food prices. Inflation accelerated to 5.3% in Italy. In many countries, the increase in energy prices on 1 January had the same effect and a residual effect will remain in February. If the news did not have a strong impact (the market still expects a 25bp rate hike from the ECB this year and the EUR/USD did not rise higher than 1.1330 before falling back to 1.13), it is because the core inflation rate fell from 2.6% to 2.3%. But this is the least we could have expected with the VAT effect in Germany and the consensus was for 2.3%!

Other important news yesterday was the fall in US private employment according to ADP figures (-301k, half of which was in the hotel and leisure sector). The plunge should normally be erased in February and March as the Omicron wave subsides. Again, little impact on the markets.

Today, we will have the services PMIs but above all, the BoE and ECB meetings. It seems almost certain that the BoE will raise its base rate again by 0.25% this time. The uncertainty concerns the size of its balance sheet: it could announce that it will reduce it very soon, as the Fed is considering doing. As for the ECB, no decision is expected, but the market will be watching for any change in its forward guidance and Mrs. Lagarde will have a hard time keeping her ultra-dovish stance.