Bond yields and the euro rebound

We spent the week noting the curious decline in bond yields while the US figures were frankly good. If they rebounded yesterday, it was not…

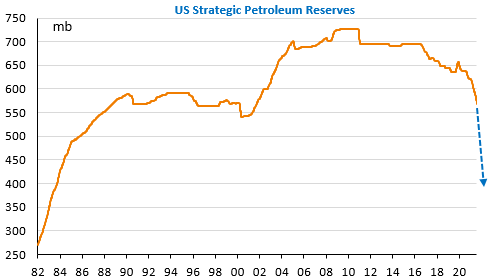

As we reported yesterday morning, the Biden Administration has announced that it will draw on its strategic reserves in a colossal way, as nearly 1mb/d of oil will be put on the market for about 6 months, or a total of 180mb.

President Biden said he hoped that allied countries could add 30-50mb of their own reserves. He also intends to put pressure on oil companies to increase production. Crude oil prices continued to fall moderately yesterday, around $108/b for Brent, before the change in the benchmark contract that brought Brent 1st-nearby to below $103/b now (a sharp drop due to strong backwardation on the short end of the forward curve). The price of the US benchmark, WTI, has fallen sharply. It is now trading around $98.5/b.

OPEC+ announced a very slightly higher production increase in May (+432kb/d), which may have accentuated the price decline, but it is mainly concerns about demand in China, Europe and the US that are also starting to be taken into account by the market.