Inflation expectations on the rise

Equity markets in Europe and the US, with the exception of the Nasdaq, continued to rise modestly yesterday, still supported by corporate earnings. But inflation…

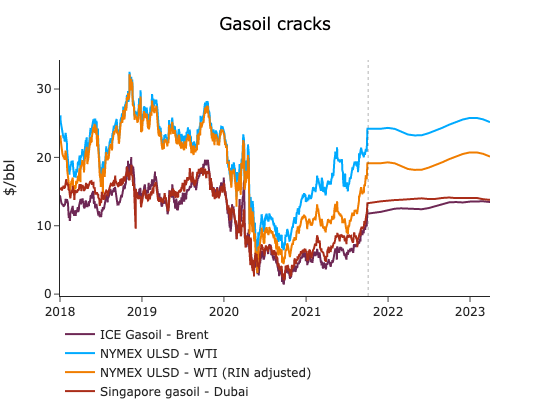

ICE Brent Dec-21 contracts continued to be supported ahead of the OPEC+ meeting, as refined product markets signalled strong demand for middle distillates and fuel oil. Global prices across the complex are healthy levels for crude and refined products. Indeed, Refiners’ margins are boosted by diesel cracks being back to pre-pandemic levels in Europe and Asia. Falling inventories in the East of Suez are boosting the global diesel scarcity as Europe is usually supplied with diesel by Asia and Russia during the winter season. Fuel oil stocks continued to be shrinking according to high-frequency weekly data in Fujairah and Singapore (-3 mb combined).

Given our current forecasted crude balance, we do not expect OPEC+ to add more supply than they previously agreed to for two reasons. First, the current agreement remains a stable equilibrium between countries, with little incentives to deviate from it and take the risk that talks collapse. Secondly, OPEC nations and our previsions anticipate crude builds in Q1 2022, as Chinese refiners’ planned outage rises seasonally during the first months of the year, leaving global inventories building by 1.1 mb/d over the first quarter.