European gas prices hit new record highs

The bullish trend in European gas prices showed no sign of abating yesterday with all contracts posting strong gains ahead of a tight supply period…

On Friday oil benchmarks moved up. ICE Brent gained 2.8% to settle at $113.12/b, while NYMEX WTI front month went 3.2% higher and closed at $107.62/b.

This move can be seen as a rebound, after the recent decline of oil prices due to the macroeconomic outlook. Indeed, the market is tight with a growing demand and a short supply.

Some support came from Libya, where the National Oil Corporation did not publish data about production. In the country, protesters are blocking oil fields and export terminals.

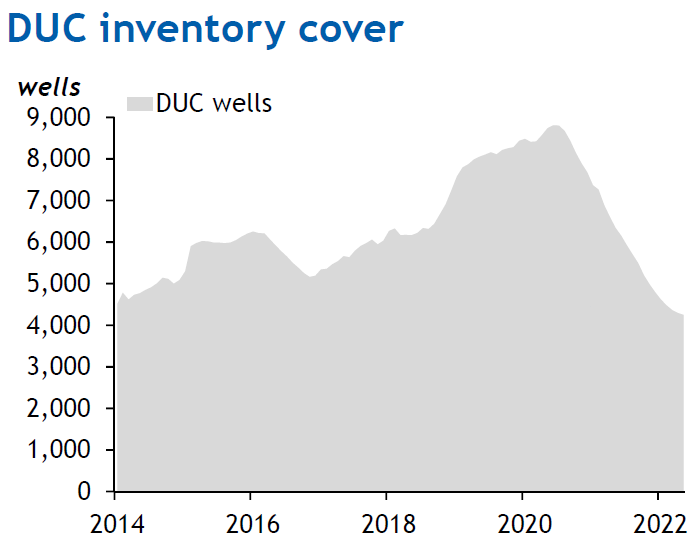

Last week the number of active rigs climbed by 10 (to 594) in the US. We can expect the number of new active rigs (and thus the US crude production) to increase more slowly now because the number of drilled-but-uncompleted wells, (that cost about 60% less to start than new wells) is declining.

This week we will have the monthly meeting of OPEC+ ambassadors, the cartel is expected to increase production quotas by 648kb/d in August. And, in Elmau, Germany, leaders of G7 countries could decide to pass new measures to sanction exports of Russian oil, one proposal is to put a price cap on oil exported from Russia. But an official said that, to be effective, this cap needs the support of India (President Modi is invited to the G7 summit) and China.

This morning oil is flat.