Maintenance on the Forties pipeline boosts Dated Brent prices

ICE Brent prompt prices rose to 68.2 $/b as the June loading program for Forties crude would only amount for two cargoes, as planned maintenance…

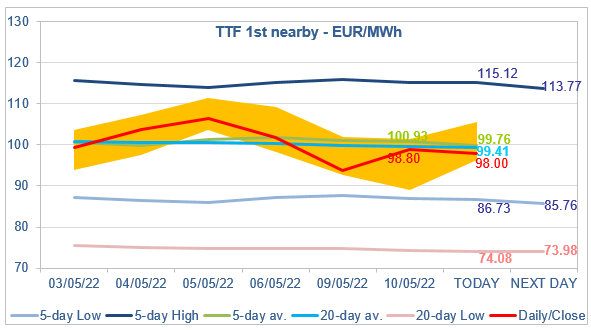

European gas prices rebounded yesterday after one of the two entry points for Russian gas transit through Ukraine stopped operating (see the news we released yesterday afternoon). And actually, Russian flows through Ukraine dropped to 81 mm cm/day on average yesterday, compared to 92 mm cm/day on Monday, driving total Russian flows to 250 mm cm/day on average, compared to 261 mm cm/day on Monday. On their side, Norwegian flows weakened to 306 mm cm/day on average yesterday, compared to 311 mm cm/day on Monday.

The drop in coal prices (-2.42% for API2 1st nearby prices, -1.75% for Cal 2023 prices) helped limit a bit the upward pressure, particularly for far curve prices.

At the close, NBP ICE June 2022 prices increased by 17.060 p/th (+13.25%), to 145.770 p/th. TTF ICE June 2022 prices were up by €5.01 (+5.35%), closing at €98.801/MWh. On the far curve, TTF ICE Cal 2023 prices were up by €1.52 (+1.94%), closing at €79.570/MWh.

In Asia, JKM spot prices dropped by 3.58%, to €62.716/MWh; June 2022 prices dropped by 0.49%, to €74.486/MWh.

Russian flows through Ukraine are nominated lower again this morning, at 66 mm cm/day. But the market seems to consider that given the current fundamentals (high LNG supply, weak demand) it is still sufficient, particularly as Norwegian flows are rebounding this morning, to 316 mm cm/day. Indeed, in their yesterday rise, TTF ICE June 2022 prices failed to close above the 5-day average and the 20-day average, finding their equilibrium at a level which is enough to limit gas demand for power generation (the maximum coal switching level was 96.35/MWh yesterday, compared to 97.68/MWh on Monday). But, if Russian supply was to fall further, panic buying by some physical participants and investors’ buying could drive prices towards the 5-day High.