Macro & Oil Report : Donald Trump takes center stage

Macro & Oil Report: Donald Trump takes center stage December, 2 2024 Macro & Oil Everything has revolved around Donald Trump since his election, including…

Almost all the activity indicators published yesterday surprised on the upside, which supported risky assets and caused a sharp decline in the US dollar, in the wake, let us recall, of good news from China. But they also reinforced expectations of monetary tightening and led to a rise in bond yields (the US 10 year is close to 3% again). In the US, retail sales rose by 0.9% over the month in April after +1.4% in March. Industrial production increased by 1.1% after +0.9% in March, while inventories rose by 2%. Eurozone GDP growth was revised up from +0.2% to +0.3% in Q1, with no change to the initial estimates for the major countries. The event came from Klaas Knot, the ECB’s Dutch central banker, who for the first time mentioned the hypothesis of a 50bp hike in key rates (in one go). This statement reinforced the rise of the euro against the USD, with the exchange rate touching 1.0564. The euro also partially erased its initial losses against the British pound after the release of UK employment figures that were well above expectations. The pound did not bounce back this morning after UK inflation figures rose sharply (9% after 7% yoy in April) but slightly less than expected. The EUR/GBP exchange rate is around 0.8450.

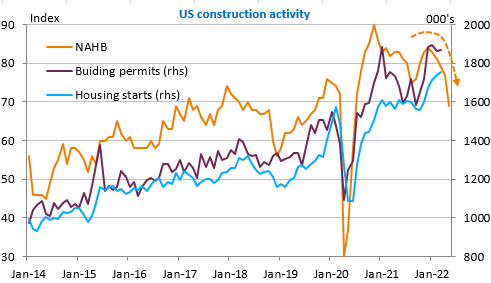

Japan’s GDP declined in Q1 but less than expected (-0.2% qoq vs. a consensus of -0.4% qoq) thanks to a good resistance of domestic demand to anti-Covid measures. The yen seems to be stabilising below 130 against the USD after its sharp fall of the last 2 months. The sharp decline in the NAHB construction index (the 5th in a row) in the US was little noted but reflects the dual impact of rising credit rates and higher material costs and foreshadows a downturn in the housing market. Housing starts and building permits are expected to fall today for the month of April. This will be the main economic report of the day with the revision of the Eurozone inflation figures.