TTF month-ahead prices hit a new 12-year high

The benchmark TTF ICE month-ahead contract (July 21) reached its highest level since October 2008 at €29.40/MWh at the close on Friday, supported by planned outages…

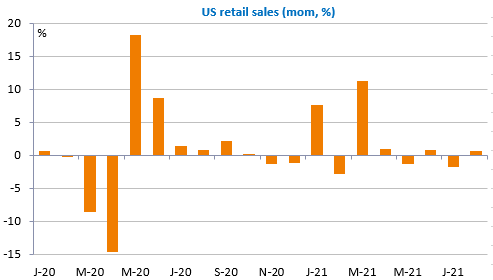

The surprise rebound in US retail sales in August (+0.7% m/m), as the variant delta extended its grip on the south and centre of the country, has reintroduced a dose of uncertainty ahead of the Fed meeting next week. What if a reduction in asset purchases is formally announced as early as Wednesday? Long-term yields rose (slightly), with the 10-year approaching 1.35%, and the dollar strengthened to 1.1750 against the euro. The US equity market was hesitant, but the rise in the dollar (among others) supported European markets.

The rebound in US retail sales is all the more surprising when compared to the further fall in UK retail sales for the 4th month in a row, despite the fact that the country seems to have weathered the latest epidemic rather well thanks to vaccination. But the restrictive quarantine measures and mobility restrictions continue to hold back activity. Expectations of a rate hike by the Bank of England in February 2022 seem excessive and the pound could suffer.

The main thing to watch today is the revision of the Eurozone’s inflation figures for August, but above all, the University of Michigan’s US consumer confidence index, in particular their inflation expectations.