Bond yields continue to rise. China reassures on the housing market

The US 10y yield reached 1.54% this morning, its highest level since June. The market is gradually integrating the prospect of monetary tightening, not only…

In less than 2 hours yesterday, the price of Brent 1st-nearby first approached $115/b before plunging towards $104/b. It has since recovered to around $113/b.

Fears of the consequences of the restrictive measures taken in Shanghai to curb the pandemic and hopes for peace in Ukraine on a rather shaky basis at the moment (see Daily Eco) explain the fall. Explaining the rise, the approach of the OPEC meeting tomorrow which is not expected to result in a change of the rule in force since July 2021 and the estimates (which we reported yesterday) that Saudi Arabia has reduced its exports quite significantly in March. It is also confirmed that Russian oil estimates point to a sharp turnaround in both exports and refinery activity around mid-March as inventories fill up. According to Bloomberg, this has already forced production to fall below 11mb/d and if current trends continue, the fall in production could be much more severe in April, possibly causing lasting damage to the country’s production capacity. It should be remembered that in its last report the IEA assumed a drop of 3mb/d. More than ever, and even if the fighting in Ukraine stops, the question of replacing Russian oil on the market arises.

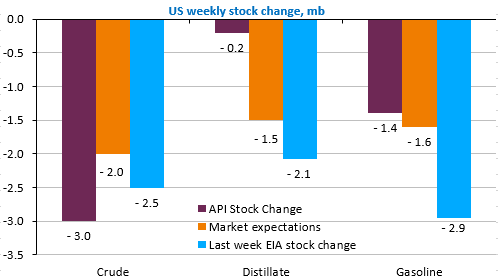

The weekly US Department of Energy statistics will be published today. According to the API estimates, crude and product inventories fell again as shown in the chart below.