2024 energy market outlook: is the energy crisis over?

The EnergyScan team held its quarterly webinar covering key trends and events on energy markets. In this webinar, our experts addressed the following topics, with…

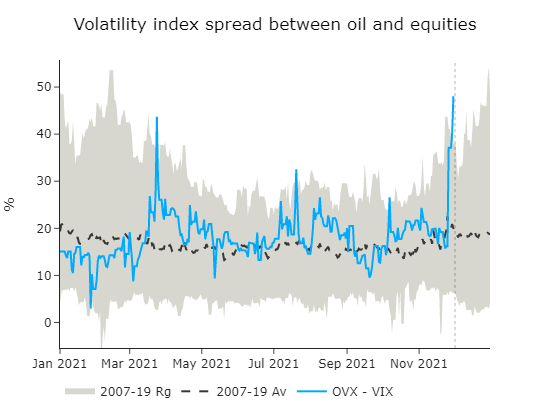

Crude prices remained volatile, with an intraday correction of 3%, to end up gaining back most of it, at 72 $/b for the February ICE Brent contract. Oil-specific volatility remained markedly above equity volatility, which has usually moved in tandem during episodes of expected downward demand revision akin to the one we are experiencing. The depressed price outlook should persist, as long as volatility remains elevated, and time spreads continue to correct to the downside, with 6-month prompt time spreads at 2.6 $/b, from 6 $/b at its peak in early November. OPEC’s meeting, likely held on Thursday, will continue to support oil volatility, as the outcome appears more uncertain than ever, given the lack of scientific data around the omicron variant.

Looking at data releases, the API survey reported a build in refined product inventories of 3 mb and a drop in crude oil inventories of 0.75 mb. In Japan, run rates are creeping higher, while commercial inventories dropped by another 4 mb w/w. Kerosene stocks are now ready for the winter, as the stock reached 17.7 mb as of last week.