Anti-Covid vaccination: from bad to worse for the EU

The main EU countries have suspended the AstraZeneca vaccine over concerns it may cause blood clots. This is another blow to the vaccination campaign in…

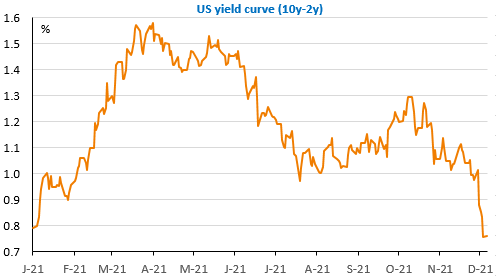

After hesitating, the US bond market decided and 10-year yields fell to 1.33%, which may seem logical given the weakness of job creation in November (+210k) compared to expectations and the surprise slowdown in wage growth to +4.8% yoy. In fact, not at all. The real reason for the drop in long rates is the conviction that nothing will stop the Fed from accelerating its monetary tightening and we can see this in the rise in the 2-year rate, which has almost wiped out the plunge following the appearance of the Omicron variant.

On the other hand, news from South Africa seems to confirm its low lethality and because of its high contagiousness, Omicron could even be good news in the long run if it helps marginalise the Delta variant. More details on possible scenarios here. On vaccine efficacy, the different laboratories continue to have quite different messages, but this becomes a secondary issue if the focus is still on tackling the Delta variant.

Coming back to the bond market, we see that the 2-10 year curve continues to flatten and very quickly, reflecting strong expectations of economic slowdown (due to monetary tightening) and therefore the fact that suddenly, for the equity market, everything has become bad news: a bad activity figure is negative (logical), a good one is just as negative as monetary policy will tighten. These trends could be reinforced at the end of the week with the release of US inflation figures for November (possibly above 7%).