Prices down on higher Russian supply

European gas prices dropped yesterday as the long-awaited rise in Russian flows seems to materialize. Indeed, Gazprom said yesterday it had started to implement a…

The US 10y yield reached 1.54% this morning, its highest level since June. The market is gradually integrating the prospect of monetary tightening, not only by the Fed, but by all central banks in the relatively near future. The Governor of the Bank of England has not ruled out a possible interest rate rise before the end of the year.

The Chinese authorities are trying to reassure the market (and succeeding for the moment) by promising to ensure “a healthy property market” that “protects the rights of homeowners”, which means they will oversee the downfall of property developer Evergrande. This does not tell us anything about the long-term impact of the property downturn on growth, and all indications are that it will be significant.

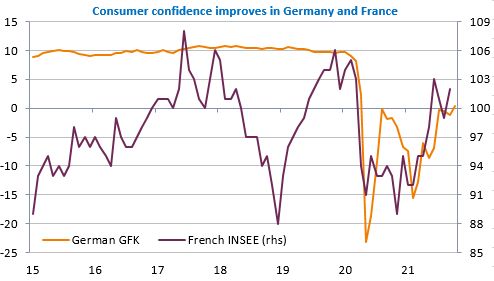

Good news in Europe this morning with the rise in household confidence in France and Germany, after a summer under the threat of the Delta variant. This does not prevent the euro from falling, as do all currencies, against the US dollar: the EUR/USD exchange rate is close to its lowest level of the year (1.1664) reached in August.

Some interesting figures today from the US, starting with consumer confidence. Of particular interest are inflation expectations. House prices are also expected to rise by more than 20% yoy, which should not calm the bond market.