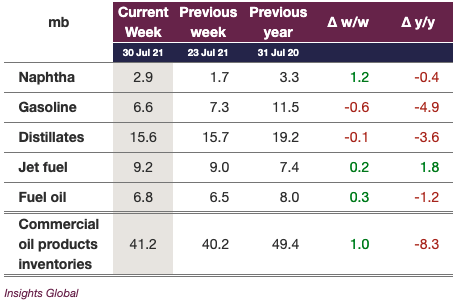

Crude oil prices in Europe and the US continued to climb, to reach 76 $/b for the ICE Brent September contract. On the opposite of the spectrum, INE crude, Shanghai’s medium sour crude future expired for September’s contract at a significantly lower level than previous trading sessions, likely to reflect the growing concerns around a recent outbreak of COVID cases in the Jiangsu province. In Europe, constructive inventory data for transportation fuels (gasoline, jet fuel and diesel) in the ARA region support crude pricing at the prompt, while Singapore inventory data showed a more uneven trajectory. Indeed, European gasoline stocks continued to draw by 0.6 mb, to drop below the 5-year average in the ARA region, while gasoil stocks declined by 0.1 mb. Naphtha stocks jumped by 1.2 mb, despite the tightness of the naphtha market. Significant backwardation in the naphtha market indicates that this upward inventory move is unlikely to persist, amid strong petrochemical margins.

ARA refined products inventories

In Singapore, gasoline stocks rose by 1.5 mb, while diesel stocks dropped by 0.5 mb. Fuel oil stocks continued to decline at a fast pace in the East of Suez – 1.5 mb – amid strong power demand, narrowing the quality spread between clean and dirty products.

The European power spot prices soared near 200€/MWh for today, buoyed by forecasts of stronger demand and weaker wind output. The day-ahead prices averaged 200.41€/MWh…

The European power spot prices continue to slowly fade yesterday, weighted by the rising renewable production. The day-ahead prices averaged 234.06€/MWh in Germany, France, Belgium…

Join EnergyScan

Get more analysis and data with our Premium subscription

Crude oil prices in Europe and the US continued to climb, to reach 76 $/b for the ICE Brent September contract. On the opposite of the spectrum, INE crude, Shanghai’s medium sour crude future expired for September’s contract at a significantly lower level than previous trading sessions, likely to reflect the growing concerns around a recent outbreak of COVID cases in the Jiangsu province. In Europe, constructive inventory data for transportation fuels (gasoline, jet fuel and diesel) in the ARA region support crude pricing at the prompt, while Singapore inventory data showed a more uneven trajectory. Indeed, European gasoline stocks continued to draw by 0.6 mb, to drop below the 5-year average in the ARA region, while gasoil stocks declined by 0.1 mb. Naphtha stocks jumped by 1.2 mb, despite the tightness of the naphtha market. Significant backwardation in the naphtha market indicates that this upward inventory move is unlikely to persist, amid strong petrochemical margins.