Crude oil prices rebound sharply after sanctions against Russia are stepped up

As explained in the Daily Eco, the EU and the US have stepped up the pressure on Russia by significantly tightening their sanctions against banks and,…

European gas prices weakened yesterday, pressured by the sharp drop in coal prices (which pulled parity prices with coal for power generation significantly down) as the Chinese government’s intervention plan to increase coal supply seems to produce effects. If these effects are confirmed, they could lead to a slowdown in Chinese LNG imports. Yesterday, Asia JKM prices were down: -3.86%, to €100.178/MWh, on the spot; -5.68%, to €98.230/MWh, for the December 2021 contract.

On the pipeline supply side, Russian flows increased slightly yesterday, averaging 258 mm cm/day, compared to 255 mm cm/day on Wednesday. Norwegian supply was slightly lower, to 342 mm cm/day on average, compared to 345 mm cm/day on Wednesday.

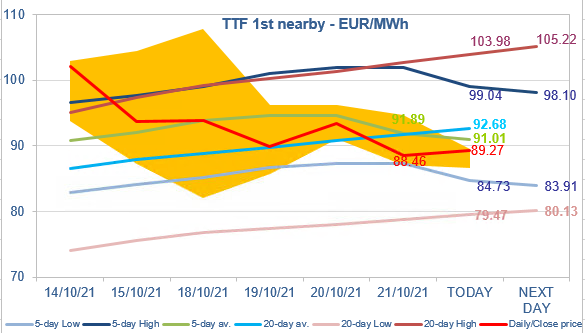

At the close, NBP ICE November 2021 prices dropped by 12.410 p/th day-on-day (-5.31%), to 221.400 p/th. TTF ICE November 2021 prices were down by €4.99 (-5.34%) at the close, to €88.463/MWh. On the far curve, TTF Cal 2022 prices were down by €2.33 (-4.12%), closing at €54.271/MWh, widening the spread against the coal parity price (€33.671/MWh, -8.26%).

Yesterday, TTF ICE November 2021 prices finally dropped below the 20-day average. But, even if the possible easing of the energy crisis in China gives rise to hopes of a more comfortable LNG supply to Europe, low stock levels and uncertainty on Russian supply remain key supportive factors. Therefore, the downside potential should be limited for the moment, with the 5-day Low as a strong support level (an intermediate level at €87.68/MWh could also lend support).