Slight downward correction

European gas prices eased slightly yesterday as the bullish momentum fueled by President Putin’s announcement that Russia will seek payment in rubles for gas sold…

It is almost certain that the Turkish Central Bank will announce a 3rd consecutive and significant rate cut today (-100 to -150bp). Since September, the key rate has plunged below the inflation rate which should soon cross the 20% mark due to the collapse of the currency: -30% since the beginning of the year vs USD and especially -23% since 3 months. The Central Bank has lost all independence and is only applying the precepts of President Erdogan (recalled yesterday) according to which high interest rates encourage inflation.

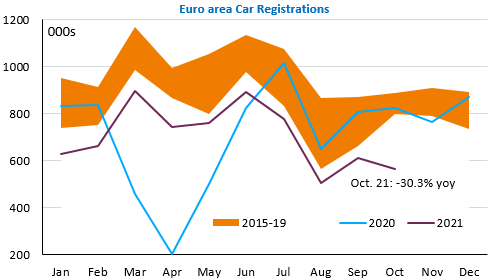

Another sharp fall in car registrations in Europe in October: the decline exceeds 30% over one year in the euro zone, whereas October 2020 was already rather low compared to the previous five years. The supply difficulties in the automotive sector show no sign of abating. They are even tending to worsen.

The economic calendar is fairly quiet until the end of the week. Long-term bond yields have fallen back a little, as have equity markets, after the sharp rise of the previous few days. Profit taking also on the dollar: the EUR/USD exchange rate goes back up to 1.1340. On the other hand, the pound is holding its gains (EUR/GBP<0.84) in anticipation of a BoE rate hike in December.