Oil Risk Premium Lifts Gas, Power and Carbon Markets

Oil Risk Premium Lifts Gas, Power and Carbon Markets May 13, 2026 Energy markets remain driven by geopolitical risk, with oil prices rising as uncertainty around the…

The European power spot prices continued to climb yesterday, buoyed by a rebound of clean fuel costs and forecasts of stronger demand, weaker nuclear availability and dropping wind production, although the higher solar and hydro generation expected today might have dampened slightly the bullish pressure. The day-ahead prices hence averaged 305.12€/MWh in Germany, France, Belgium and the Netherlands

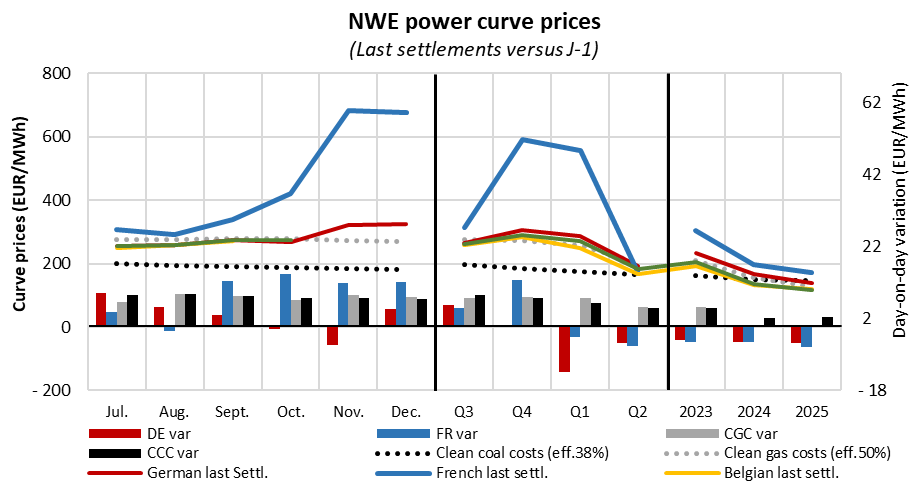

The power curve prices were mixed on the first session of the week, the short-term contracts posting moderate gains following fuel moves while the long-term faded further despite firmer gas, coal and carbon underlying contracts. Uncertainties perhaps emerged from the numerous news from the regulatory side, with Germany deciding to accelerate its original plan to save gas while the Dutch economy minister announced it will put the gas system into “early warning”, lift the cap on running hours for coal units and leave Groningen producing gas in 2022.

Germany indeed set out plans to bring back 10GW of lignite, coal and oil plants in order to reduce gas consumption, which lifted the carbon prices yesterday morning. The Parliament will decide on the legislation on July 8th which, if ratified, could enter into force in August. After their early upward move, the EUAs however steadied for the remainder of the session as most market participants seemed to wait for the Parliament plenary’s vote and quarterly options expiry, both taking place on Wednesday. The EUA Dec.22 closed at 84.00€/t, +1.63€/t from Friday’s settlement. Both gas and equity market are opening today’s session on a bullish tone, which could provide some support to the carbon market in the upcoming hours, although limited moves are expected ahead of the previously-mentioned events.