Diesel supply and demand shocks

Diesel cracks are soaring globally, which may indicate that there is stronger demand, partly due to oil-to-gas switch and a recovery in aviation demand that reduces…

European gas prices rebounded strongly yesterday, supported by cold weather, ongoing concerns on Russian supply and technical buying. The rise in Asia JKM prices (+3.01% on the spot, to €109.470/MWh; +4.14% for January 2022 prices, to €109.548/MWh) helped accompany the bullish momentum. On the pipeline supply side, Norwegian flows were almost stable yesterday, at 349 mm cm/day on average, compared to 350 mm cm/day on Friday. The same for Russian supply, which averaged 285 mm cm/day, compared to 284 mm cm/day on Friday.

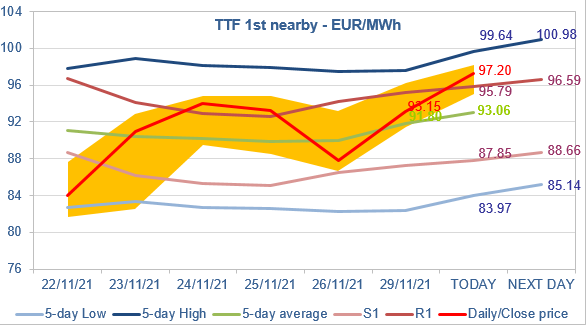

At the close, NBP ICE December 2021 prices increased by 13.960 p/th day-on-day (+6.29%), to 236.040 p/th. TTF ICE December 2021 prices were up by €5.37 (+6.12%) at the close, to €93.146/MWh. On the far curve, TTF Cal 2022 prices were up by €2.18 (+4.07%), closing at €55.733/MWh, with the spread against the coal parity price (€36.266/MWh, -3.33%) widening.

Yesterday, the R1 level opposed a resistance to TTF ICE December 2021 prices and they finally closed (and expired) below this level. But prices for the new 1st nearby (the January 2022 contract) are breaking this resistance this morning, which seems normal: in terms of fundamentals, January should be tighter than December, and Asia JKJM prices also offer upside. But, to avoid overbuying, the rise should stop at the 5-day High (or before).