Oil stable yesterday, falls this morning

Yesterday, oil continued to climb back, NYMEX WTI contract for August delivery (now the front month), that did not trade on Monday, gained +1.4% to…

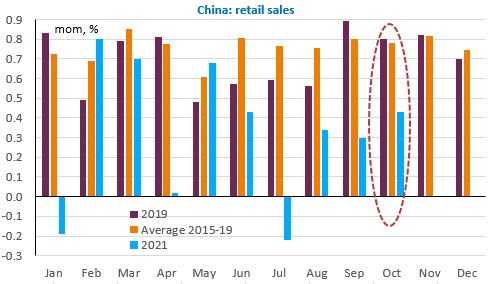

Activity seemed to accelerate in China in October: +3.5% after +3.1% yoy for industrial production and +4.9% after +4.4% yoy for retail sales. In fact, only industrial production returned to normal growth for the month, as the energy supply problems were resolved. But the chart below clearly shows that this is not the case for retail sales, as the pandemic continues to restrict household consumption.

In Japan, GDP contracted sharply in Q3 (-0.8% qoq), which is fuelling some… optimism in anticipation of a new stimulus package, the contours of which are expected to be specified this week.

On the other side of the Atlantic, inflation is undermining consumer morale according to the University of Michigan survey: the US confidence index fell to its lowest level in 10 years, while one-year inflation expectations reached their highest level since July 2008. The US 10-year yield stabilised around 1.55% and the USD held its gains against the euro (EUR/USD @ 1.145).

Today’s events include the Eurozone’s external trade report, Mrs. Lagarde’s appearance before the European Parliament and the Philadelphia Fed’s index. Key figures expected from the US and the UK this week.