Central bank week

All major central banks and even the Bank of Russia or the Bank of Turkey are meeting this week. The Bank of Turkey is expected…

European gas prices weakened overall on Friday, pressured by milder weather and steady pipeline flows. Norwegian flows were up on Friday, averaging 344 mm cm/day, compared to 338 mm cm/day on Thursday. Russian supply was almost stable, at 280 mm cm/day on average, compared to 281 mm cm/day on Thursday. The drop in Asia JKM prices (-1.83% on the spot, to €103.447/MWh; -3.32% for the January 2022 contract, to €103.122/MWh) also exerted downward pressure.

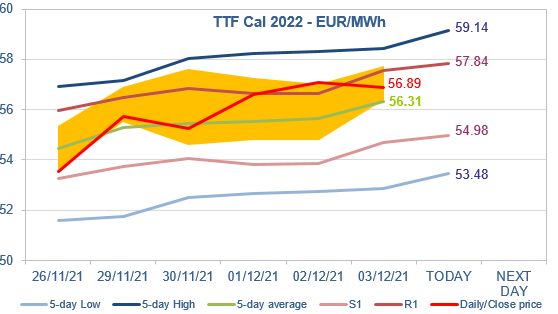

At the close, NBP ICE January 2022 prices dropped by 13.190 p/th day-on-day (-5.45%), to 228.900 p/th. TTF ICE January 2022 prices were down by €5.35 (-5.64%) at the close, to €89.478/MWh. On the far curve, TTF Cal 2022 prices were down by 17 euro cents (-0.29%), closing at €56.892/MWh, with the spread against the coal parity price (€36.986/MWh, -2.60%) slightly widening.

TTF ICE January 2022 prices closed on Friday slightly below the S1 support level. But Cal 2022 prices were much more resilient, closing between the 5-day average and the R1 level, as Q2 2022, Q3 2022 and Q4 2022 prices were up, narrowing the (huge) spread against Q1 22 prices. January 2022 prices are down again this morning, seeming to head toward the 5-day Low. As for Q2, Q3 and Q4 2022 prices, they should continue to be immune from a significant drop, as the expected gradual closure of the spread against Q1 2022 prices should continue to attract buying interests. As a consequence, the downward potential on the whole Cal 2022 contract seems limited for the time being (to the S1 level?).