Prices maintained their short term downtrend

European gas prices dropped significantly yesterday, still pressured by above-normal temperatures and more comfortable supply. Norwegian flows rebounded to 337 mm cm/day on average yesterday,…

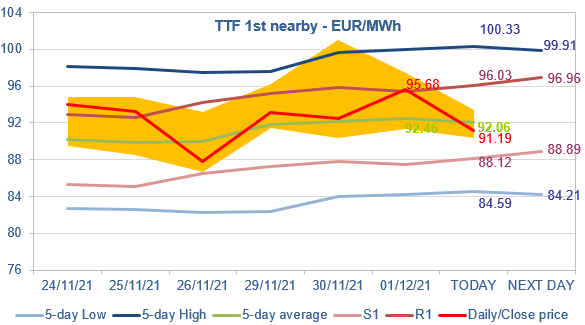

European gas prices increased yesterday, supported by strong demand due to cold weather and lower pipeline supply. Indeed, Norwegian flows were down yesterday, at 339 mm cm/day on average, compared to 346 mm cm/day on Tuesday. The same for Russian supply, which averaged 281 mm cm/day, compared to 286 mm cm/day on Tuesday. However, the moderation in Asia JKM prices (-5.23% on the spot, to €106.260/MWh; -0.02% for the January 2022 contract, to €108.177/MWh) contributed to limit the price rise.

At the close, NBP ICE January 2022 prices increased by 6.220 p/th day-on-day (+2.61%), to 244.530 p/th. TTF ICE January 2022 prices were up by €3.16 (+3.42%) at the close, to €95.675/MWh. On the far curve, TTF Cal 2022 prices were up by €1.34 (+2.43%), closing at €56.597/MWh, with the spread against the coal parity price (€37.259/MWh, +6.88%) narrowing.

TTF ICE January 2022 prices closed yesterday around the R1 resistance level. They are down this morning, probably pressured by profit taking. But in a context Europe still needs significant LNG volumes (as Russian supply remains low), the strong levels of Asia JKM prices should limit the downside potential. Therefore, the 5-day average should lend support; if it is broken, the decline should still stop at the S1 level.