Gas & Power Report: Energy prices shrug off winter chill and move further down in Europe

Energy prices shrug off winter chill and move further down in Europe Gas & Power #85 Despite a cold snap hitting Europe, wholesale gas and…

It was to be expected: the simultaneous emergence of the Omicron variant and the peak of inflation (the inflation rate in the euro zone reached 4.9% in November!) is confusing the financial markets. After Moderna’s CEO’s statements on the probable ineffectiveness of existing vaccines against the new variant, other less pessimistic comments from other laboratory managers gave some hope. But this was without counting on Jerome Powell who, in front of the US Senate, declared that it was time to recognise that inflation was not “transitory” and that he was therefore in favour of speeding up the pace of the Fed’s asset purchases: the stock markets fell sharply in the wake of this.

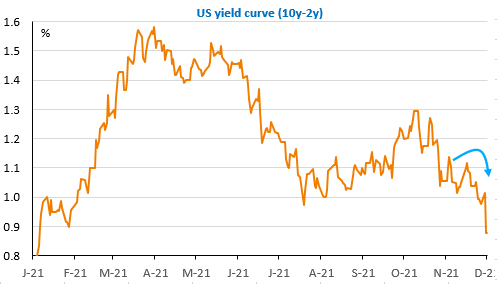

However, the flattening of the yield curve (the US 2-year rate rose by 8bp while the 10-year rate fell by 5bp yesterday) shows that the markets believe that the Fed will be able to control inflation.

Moreover, in the current context, monetary tightening is not necessarily bad: we saw this again yesterday with the fall in the Conference Board’s consumer confidence index due to a surge in inflation expectations. The stock markets could start to rise again today. The EUR/USD exchange rate is very volatile: it fluctuated between 1.1383 and 1.1236 yesterday and seems to be rebounding this morning.

The day’s calendar is full of manufacturing PMIs and ISM in the US, the ADP report on US private employment and the OECD outlook. Retail sales fell again in Germany in October.