Power prices rose as EU planned ban on Russian coal imports

The power spot prices faded in north western Europe yesterday, pressured by forecasts of stronger wind and solar output, weaker demand and increasing Belgian nuclear…

European gas prices increased yesterday, supported by the results of the monthly gas transmission capacity auctions with Gazprom not booking additional capacity into Western Europe. The market ignored the increase in spot pipeline supply, probably worried about the upcoming fall in Norwegian flows. Norwegian flows rebounded to normal yesterday, to 346 mm cm/day on average, compared to 282 mm cm/day on Friday. Russian supply was also up, averaging 288 mm cm/day, compared to 276 mm cm/day on Friday. The rise in Asia JKM prices (+3.78%, to €94.183/MWh, on the spot; +0.88%, to €94.893/MWh, for the December 2021 contract) and in parity prices with coal for power generation (thanks mainly to EUA prices) helped accompany the bullish momentum.

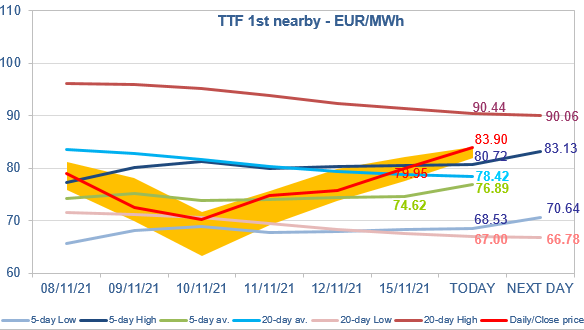

At the close, NBP ICE December 2021 prices increased by 10.740 p/th day-on-day (+5.53%), to 204.790 p/th. TTF ICE December 2021 prices were up by €4.27 (+5.65%) at the close, to €79.947/MWh. On the far curve, TTF Cal 2022 prices were up by €1.48 (+3.08%), closing at €49.650/MWh, and the spread against the coal parity price (€33.448/MWh, +2.81%) widened.

The 5-day High managed to curb the upward pressure yesterday, TTF ICE December 2021 prices finally closing slightly below this resistance level. But this resistance is being broken this morning, the combination of lower Norwegian flows (down to 311 mm cm/day due to a planned maintenance on the giant Troll field) and the disappointment on the level of Russian supply now feeding a bullish momentum. Profit taking by the 5-day actors can still limit the upward pressure today, but the risk is now on the upside.