The Fed calms things down

Equity markets continue to rally; the S&P 500 has erased half of its losses. US long rates stabilised as Fed members tried to put out the…

European gas prices were mixed yesterday, torn between ongoing concerns on supply and profit taking. Yesterday, reflecting the problems on the compressors mentioned the previous days, Russian supply weakened again, averaging 106 mm cm/day (compared to 136 mm cm/day on Wednesday), with Nord Stream 1 flows down to 70 mm cm/day, compared to 166 mm cm/day early June. And a senior Russian official raised the possibility of a total halt in Nord Stream 1 flows in case of further problems with maintenance on the turbines.

On their side, Norwegian flows weakened slightly, averaging 312 mm cm/day on average, compared to 318 mm cm/day on Wednesday.

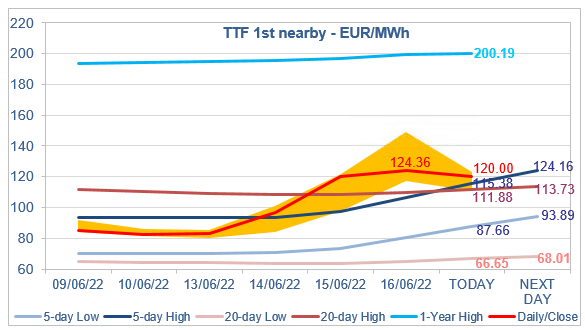

At the close, NBP ICE July 2022 prices dropped by 24.160 p/th (-9.37%), to 233.620 p/th, equivalent to €93.430/MWh. TTF ICE July 2022 prices were up by €4.032 (+3.35%), closing at €124.364/MWh. On the far curve, TTF ICE Cal 2023 prices increased by 32 euro cents (+0.35%), closing at €91.238/MWh.

In Asia, JKM spot prices increased by 33.37%, to €124.814/MWh ; August 2022 prices increased by 2.20%, to €112.099/MWh.

The rise in TTF 1st nearby prices was more moderate yesterday. Indeed, with prices above the 5-day High and the 20-day High targets, some financial participants have probably decided to take their profits. But, the strong upward reaction of Asia JKM spot prices tend to show that Asian buyers do not intend to totally abandon available flexible LNG cargoes to their European counterparts, although it remains to be seen whether this interest will last (August prices are lower).

Prices are weakening this morning, continuing their technical correction. But given the very bullish (5-day) trend, the drop should be limited.