European prices mixed yesterday

European gas prices were mixed yesterday, torn between the impacts of ongoing tight balances on the one hand and profit taking by financial participants on…

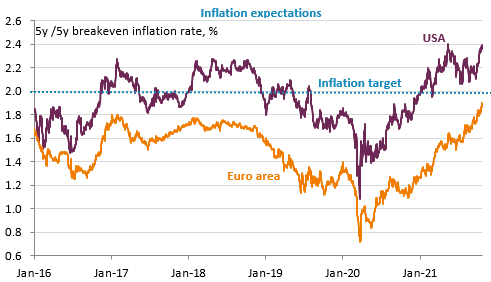

Equity markets in Europe and the US, with the exception of the Nasdaq, continued to rise modestly yesterday, still supported by corporate earnings. But inflation expectations are increasing and bond yields remain close to their recent highs.

The Fed’s Beige Book delivered a state of play of the US economy tinged with risks of stagflation: “modest to moderate” growth, constrained by bottlenecks and inflationary pressures clearly on the rise with a labour market where the balance of power has reversed: not only are companies struggling to recruit but they are unable to retain their employees. As a result, wages are accelerating.

In China, the resolution of the Evergrande crisis does not seem to be going well and the markets took a hit last night. This time, caution should also be exercised in Europe and the US.

The economic agenda is quite full today, but without any key indicators: the INSEE survey in France showed a stable business climate in industry but a clear improvement in services. We are expecting a number of economic reports in the United States: jobless claims, the Philadelphia Fed index, existing home sales, leading indicators, etc. The dollar continues to slide slowly against the euro towards 1.1650.