The Fed’s minutes: nasty surprise or relief?

The Fed Minutes included a key sentence showing that some members are ready to start discussing the tapering of bond purchases, provided the economic recovery…

Front-month time spreads flipped in shallow contango for the first time since Q4 2020, a worrying sign that conflicts with the fundamental data we are collecting, whether it is in inventories or demand data. Indeed, satellite data shows a continued decline in onshore inventories (-10 mb for the first 15 days of December according to Kayyros), and we expect the December stock draws to continue. ICE Brent’s G/H time spreads might price a rapidly shifting market as soon as Chinese runs decline in January and February, but we still struggle to see this contango as justified.

The US API survey showed slow builds in gasoline stocks, of 0.43 mb, while diesel and crude oil stocks declined by 1.8 mb. The expected increase in gasoline stocks at this time of the year is usually 3-4 mb. Higher than expected US gasoline demand could be the culprit, which could be an unforeseen bullish factor for US gasoline markets.

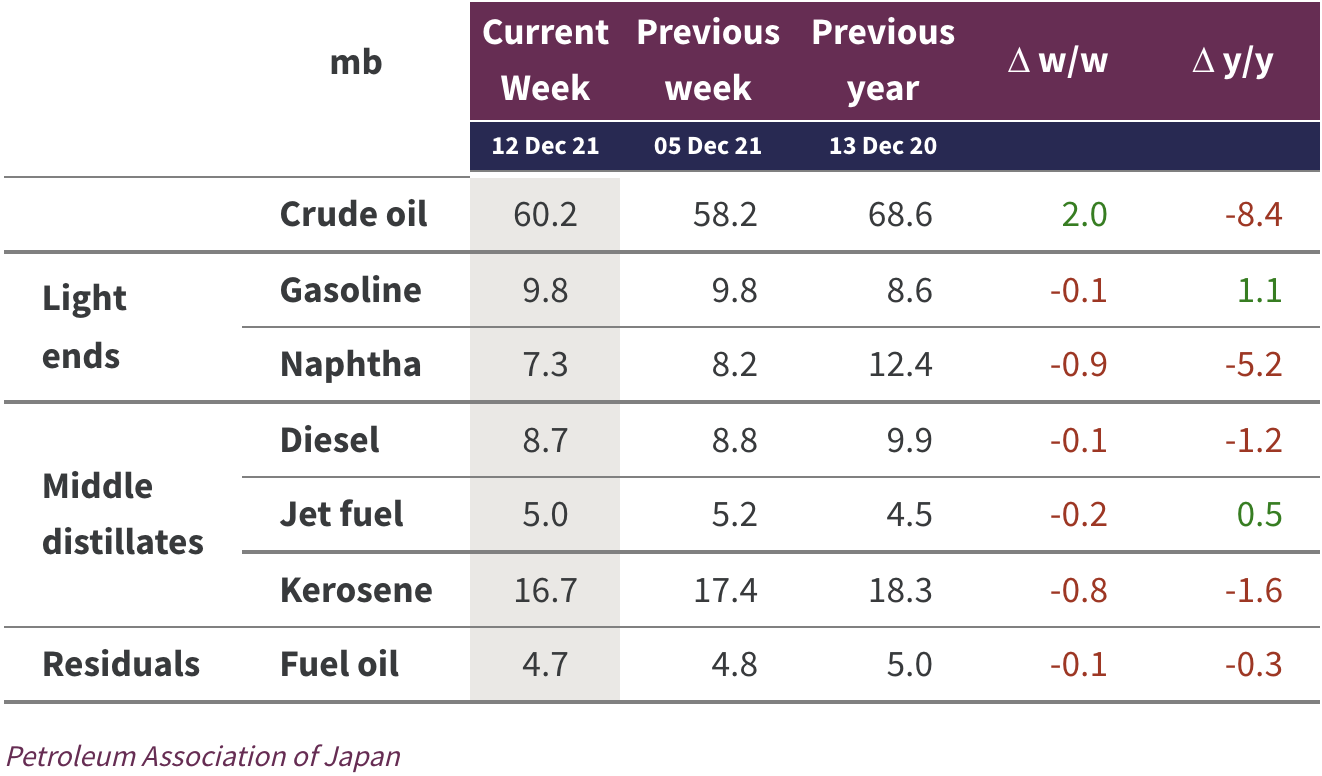

Chinese refining runs expanded at a much faster rate than previously anticipated, with November’s throughout at 14.5 mb/d, as state-owned refiners responded to localized diesel shortages by running diesel-making units harder than in October. weekly Japanese runs also recovered further, right on our forecast, at 2.88 mb/d last week. While commercial Japanese crude oil stocks grew by 2 mb w/w, refined products stocks dropped by more than this amount. The overall refining runs and stocks outlook in Asia appear to be markedly more bullish than what time spreads would suggest today.

Japanese weekly stocks