The market remains bullish despite headwinds

The price of Brent 1st-nearby rose above $90/b yesterday even as US crude oil inventories rose for the second week in a row: +2.4mb. But it…

European gas prices were up overall yesterday, still supported by uncertainties on Russian supply and LNG flows (following the shutdown of the US Freeport LNG terminal and the disruption of loadings at the Shell’s Prelude FLNG terminal in Australia). The rise in coal prices (+1.88% for API2 1st nearby prices, +1.50% for Cal 2023 prices) helped accompany the bullish momentum.

On the pipeline supply side, Russian flows remained stable yesterday, at 104 mm cm/day on average. Norwegian flows dropped very slightly to 320 mm cm/day on average, compared to 322 mm cm/day on Wednesday.

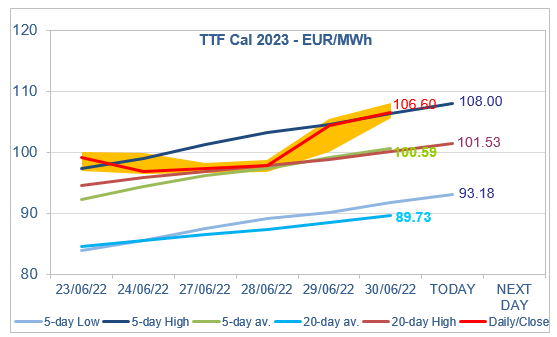

At the close, NBP ICE August 2022 prices increased by 3.480 p/th (+1.42%), to 248.300 p/th, equivalent to €98.436/MWh. TTF ICE August 2022 prices were up by €4.338 (+3.09%), closing at €144.514/MWh. On the far curve, TTF ICE Cal 2023 prices increased by €2.220 (+2.13%), closing at €106.596/MWh.

In Asia, JKM spot prices increased by 2.69%, to €128.996/MWh; August 2022 prices increased by 4.04%, to €125.848/MWh.

Like on Wednesday, TTF Cal 2023 prices closed yesterday at a level almost identical to the 5-day High. In the absence of a decisive fundamental element, this level (€108.00/MWh for today) should continue to set a resistance. At the same time, profit taking by financial participants could drive prices down, but a drop to the 5-day average or the 20-day High (€101.53/MWh) will be difficult to reach; the intermediate R1 level (€105.11/MWh) seems more attainable.