Short-squeeze drove EUA prices near 90€/t

The European power spot prices inched up yesterday, buoyed by higher clean fuel costs and forecasts of weaker French nuclear availability and German wind production.…

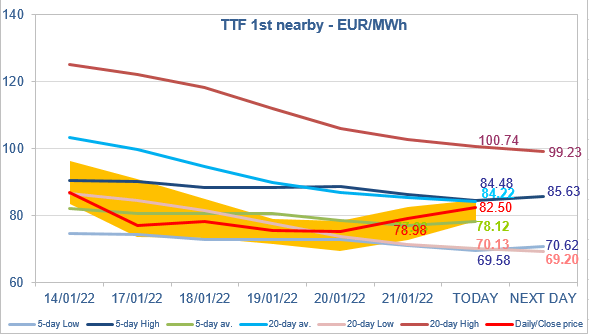

European gas prices increased on Friday as concerns about low stock levels have returned to the fore (on 22 January, European gas storages were 43% full on average, compared to 57% in 2021 and 77% in 2020). The rise in Asia JKM prices (+6.34% on the spot, to €62.903/MWh; +7.34% for the March 2022 contract, to €66.468/MWh) helped accompany the bullish momentum. On the pipeline supply side, Norwegian flows continued to rebound, reaching 342 mm cm/day on Friday, compared to 332 mm cm/day on Thursday. Russian supply remained stable at 183 mm cm/day on average.

At the close, NBP ICE February 2022 prices increased by 10.180 p/th day-on-day (+5.68%), to 189.310 p/th. TTF ICE February 2022 prices were up by €3.78 (+5.02%), closing at €78.980/MWh. On the far curve, TTF ICE Cal 2023 prices were up by €1.18 (+2.70%), closing at €44.729/MWh.

TTF ICE February 2022 prices are rising again this morning, but they are facing a double resistance: the 20-day average and the 5-day High. Normally, they should weaken now (despite their Friday rebound, Asia JKM prices continue to show a discount compared to European prices). But, the European gas equilibrium remains fragile and any new disruption on supply (from Russia or Norway in particular) could cause prices to break through the resistance levels.