American diesel pull resumes

ICE Brent front-month settled at 88.4 $/b, as the API survey showed small builds in commercial crude (1.4 mb) which counterbalanced perfectly the release of…

European gas prices dropped yesterday, pressured by mild weather, ongoing strong LNG supply and rebound in pipeline flows. Indeed, Russian supply rebounded yesterday, averaging 231 mm cm/day, compared to 217 mm cm/day on Wednesday. Norwegian flows also rebounded to 339 mm cm/day on average, compared to 325 mm cm/day on Wednesday. The drop in coal prices (although offset by higher EUA prices) also sent a bearish signal.

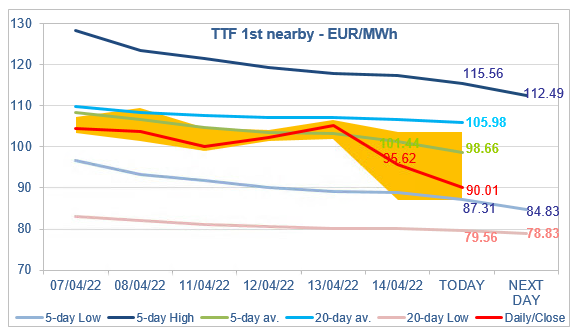

At the close, NBP ICE May 2022 prices dropped by 35.840 p/th day-on-day (-16.82%), to 177.250 p/th. TTF ICE May 2022 prices were down by €9.70 (-9.21%), closing at €95.620/MWh. On the far curve, TTF ICE Cal 2023 prices were down by €4.93 (-5.90%), closing at €78.527/MWh.

In Asia, JKM spot prices increased by 0.81%, to €92.639/MWh; May 2022 prices increased by 0.55%, to €103.780/MWh. June 2022 prices dropped by 12.02%, to €79.938/MWh.

The maximum coal switching level was almost stable yesterday, around €98/MWh. But the fact that coal prices have fallen, although moderately (-1.27% for API2 1st nearby prices, -1.33% for Cal 2023 prices), is sending some messages: coal import needs are probably weakening (in Asia and in Europe), for sure because of seasonality in power consumption, but also because of the COVId-19 induced restrictions in China; after the first moments of panic following the bans on Russian coal, global supply is adapting, optimizing the flows and sending them to the markets that need them the most, in particular European countries, Japan and South Korea. The relatively low level of Asia JKM June 2022 prices effectively suggests that Asian buyers do not intend (need) to outbid against their European counterparts.

Overall, TTF ICE May 2022 prices are down again this morning, but the 5-day Low is lending them support. Any tightness on fundamentals could bring them back to the 5-day average (which is very close to the maximum coal switching level) or the 20-day average.