And now the French nuclear crisis

The European energy crunch entered a new phase on Thursday with an extreme spike in French power prices mirroring similar moves observed in Japan or Texas…

The temporary deal on the US debt ceiling also gives the Democrats time to agree on the stimulus packages that the Biden administration wants to push through. This may explain why the markets reacted so favourably to the lifting of a risk they never really took seriously (a US default). The sharp rebound in China’s services PMI in September (from 46.7 to 53.4) also reassures that domestic demand will be strong when the containment measures are lifted.

But on the other hand, this good news immediately puts pressure on commodity prices and pushes up yields (the 10-year is close to 1.60%, the highest in 4 months), precisely the reasons that led to the equity market correction in September…

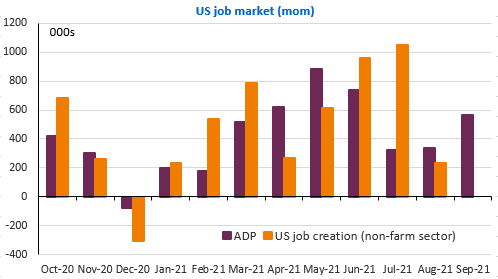

The US job report will be the main event of the day: barring a huge surprise, job creation will be sufficient to justify an announcement of a reduction in the Fed’s asset purchases as early as November 3rd. The risks are more on the upside for bond yields and the prospect of a Fed funds rate hike as early as 2022. The best is the enemy of the good…

The EUR/USD exchange rate is stable around 1.1550.