European gas prices extended gains

European gas prices increased again yesterday, supported by forecasts of lower temperatures from tomorrow with levels expected to drop significantly below normal next week. While…

European gas prices rebounded yesterday during a session marked by low volatility. The slight increase in Asia JKM prices (+1.27%, to €104.205/MWh, on the spot; +1.76%, to €104.146/MWh, for the December 2021 contract) and in parity prices with coal for power generation (the strong rise in EUA prices offset the drop in coal prices) provided some support.

On the pipeline supply side, Russian flows were almost stable yesterday, averaging 255 mm cm/day, compared to 256 mm cm/day on Tuesday. Norwegian supply was very slightly lower, to 345 mm cm/day on average, compared to 348 mm cm/day on Tuesday.

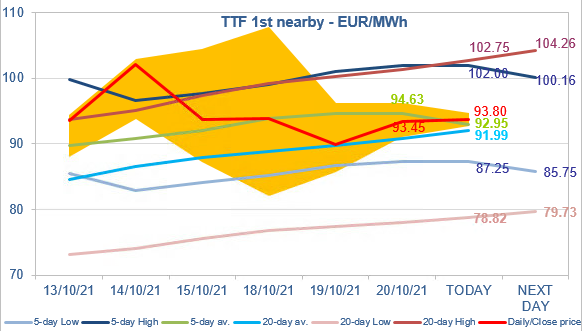

At the close, NBP ICE November 2021 prices increased by 7.900 p/th day-on-day (+3.50%), to 233.810 p/th. TTF ICE November 2021 prices were up by €3.52 (+3.91%) at the close, to €93.451/MWh. On the far curve, TTF Cal 2022 prices were up by €1.22 (+2.21%), closing at €56.604/MWh, widening slightly the spread against the coal parity price (€36.703/MWh, +2.01%).

Yesterday, TTF ICE November 2021 prices traded throughout the session above the 20-day average. As we think European fundamentals do not justify for the moment the emergence of a downtrend, this 20-day average could continue to lend strong support today. However, although there are still a lot of concerns about Russian supply, the current drop in coal prices in China (after the government signaled intervention to increase supply) could impact the LNG market and ultimately exert a downward pressure on European prices. Therefore, a drop below the 20-day average cannot be totally excluded.