Mr. Biden’s inauguration as president marks a return to normalcy

On his first day as president, Mr. Biden signed a series of executive orders unwinding the most controversial aspects of the previous administration’s policy. Financial…

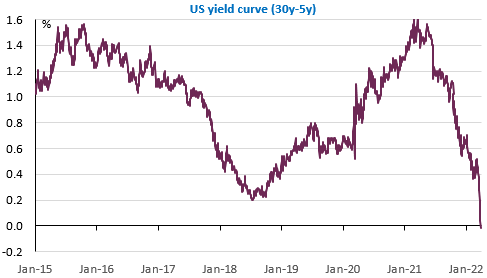

The markets are now assuming the equivalent of almost 9 25bp rate hikes by the Fed by the end of the year, i.e. out of the 6 remaining meetings, 3 would see the Fed raise rates by 50bp. The extraordinary (because it really is an extreme scenario from a historical point of view) has become the central scenario. The entire US yield curve is flattening: between 5y and 2y, there is only 25bp and between 10y and 2y, only 15bp. The curve has just inverted between 30y and 5y. This has not happened since 2006 and in the past, within 1 or 2 years, a recession has always followed. Perhaps this means that the market is far too aggressive in its expectations of monetary tightening and that the Fed will slow the pace of rate hikes well as soon as the first tangible signs of weakening growth appear. But in any case, the fact that the S&P 500 was up nearly 2% last week after a 6% rise the week before raises questions, to say the least.

The markets will continue to scrutinise the situation in Ukraine and whether the Russian army is now focusing on annexing the Donbass provinces, leaving the rest of the country behind. But the economic calendar is full of data, including the employment report and the ISM manufacturing report at the end of the week in the United States, as well as consumer confidence and household consumption. There will also be Chinese PMIs with the risk of the pandemic having a significant impact on activity and finally the European Commission survey and inflation figures in the Eurozone. All of which will fuel high volatility in the markets.