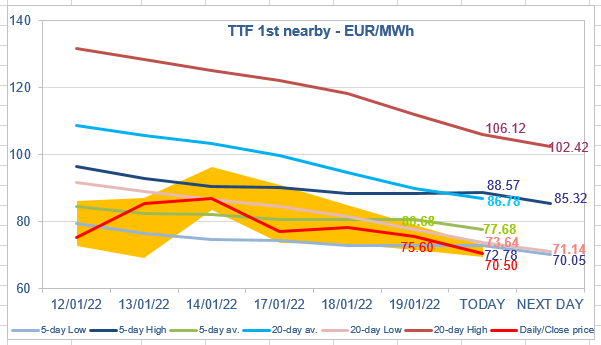

Prices up after certification procedure of Nord Stream 2 AG was suspended

European gas prices increased strongly yesterday, supported by the Germany’s energy regulator (the Bundesnetzagentur) to suspend the procedure to certify Nord Stream 2 AG as…