Power and carbon prices rose alongside the gas market

The power spot prices edged down in northwestern Europe yesterday, pressured by forecasts of better French nuclear availability and sharply rising wind output, despite higher…

Equity markets continue to yo-yo: as expected, they rebounded in the US, but European markets adjusted on the previous day’s US decline. It seems that the initial pessimism linked to the appearance of the Omicron variant is dissipating somewhat and that the markets are returning to a more neutral position, awaiting the first serious studies on the subject.

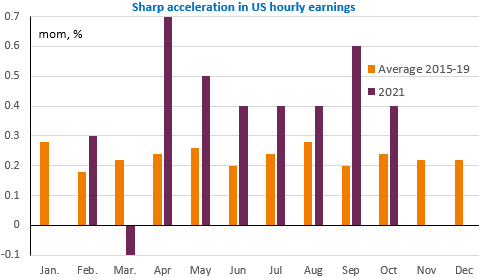

Long-term yields remain close to their recent lows, with the US 10-year just above 1.4%. This partly reflects these concerns about Omicron, but more importantly, the sharp tightening of rhetoric from Fed members which has resulted in a flattening of the yield curve, via both a rise in short-term yields and a fall in long rates. The bond market will be tested today by the release of US employment figures: strong job creation is expected on the back of good ADP private employment figures and confirmation of the decline in weekly jobless claims (222k yesterday), but more importantly, wages are expected to continue to accelerate, giving the feeling that the Fed’s wake-up call is long overdue and that it may need to tighten policy further to control inflation.

The dollar has started to rise against the euro (EUR/USD < 1.13). This rebound could gain momentum with today’s figures: the US employment report, the (disappointing) Eurozone retail sales and the PMIs and ISM in services.