ICE Brent prompt contract collapsed further yesterday, at 73.2 $/b for the September contract. The move was likely caused by two drivers:

A broad selloff in commodity futures, as inflation hedges were less demanded by financial players, given how global bond markets are rallying, with the 10Y T-bond at 1.3% and inflation expectations consistently declining since June (the 5Y breakeven inflation between nominal and TIPS),

Aggressive put hedging from US producers, for 2022 and 2023, which are then delta-hedged by option underwriters at more prompt, liquid maturities.

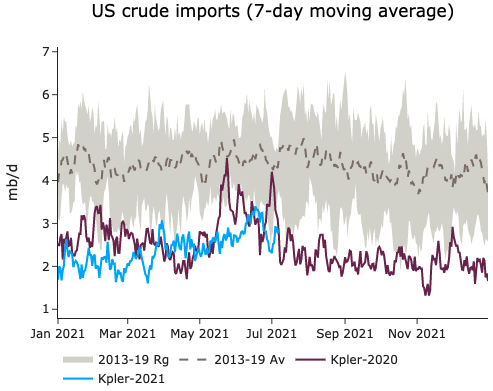

On the fundamental side, the API survey and Kpler are both recording steep draws in the US crude market, with a decline of 8 mb last week. More interesting, gasoline stocks dipped by about 2 mb according to the API survey, after few weeks of builds due to elevated imports from Europe. US imports from the Gulf coast are also finally ramping up according to satellite data, in line with the WTI-Brent spread recent narrowing. The EIA report due today should give us more insights into the US markets.

European gas prices dropped significantly yesterday, pressured by more comfortable pipeline supply and profit taking after the previous sessions’ strong gains. Russian flows were stable…

ICE Brent prompt contract collapsed further yesterday, at 73.2 $/b for the September contract. The move was likely caused by two drivers:

On the fundamental side, the API survey and Kpler are both recording steep draws in the US crude market, with a decline of 8 mb last week. More interesting, gasoline stocks dipped by about 2 mb according to the API survey, after few weeks of builds due to elevated imports from Europe. US imports from the Gulf coast are also finally ramping up according to satellite data, in line with the WTI-Brent spread recent narrowing. The EIA report due today should give us more insights into the US markets.