European prices down amid lower storage withdrawals

European gas prices weakened on Friday, apparently under pressure from the rebound in Norwegian supply (to 348 mm cm/day on average, compared to 341 mm…

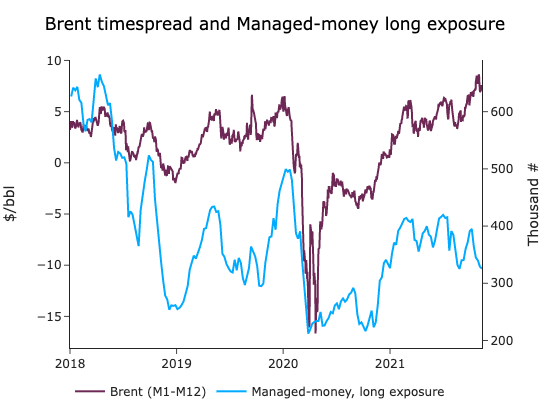

Crude prices remained pressured, sticking to the 80-82 $/b range, as the possibility of a US SPR release limited prompt tightness. With such growing political pressure and uncertainty, money managers continued to cut their exposure to major futures markets (Brent, WTI). The Brent open interest from financial players declined by 94k since this summer when the reflation trade narrative remained intact. The Biden administration may release stocks imminently, which would be at odds with previous releases, where a supply disruption needed to be identified for activating such release. Furthermore, Biden’s view that petroleum markets could cope with Iranian crude being off the market added another layer of fogginess to the US energy policy. The fact that outright crude prices are stagnating below 85 $/b is also a deterrent for the administration to act.

On the Chinese side, refiners processed more crude in October, at 13.64 mb/d. Yet, it remains markedly below its peak in June 2021, at 14.6 mb/d. There is evidence that refining runs will continue to strengthen. Sinopec and PetroChina both mentioned their ramp-up in diesel output by close to 20%, amid rising domestic prices and improving margins. Shandong independent refiners were also raising their outputs compared to October, closer to a 73% utilization rate.