Fed’s chairman cements an aggressive monetary tightening

Jay Powell, the US central bank head, declared at a panel hosted by the IMF yesterday that a 50 basis points interest rate hike was on…

US equity markets fell back yesterday as interest rates rose to above 3.2% for the US 10 year. Market participants appear unconvinced as we approach the end of the month, with recession fears pitted against inflation fears to determine what central bank policy will be. US durable goods orders rose again in May (+0.7% mom) as did pending home sales, beating expectations. In contrast, the Dallas Fed index plunged. However, the market trend reversed again in Asia on the back of an easing of anti-covid rules in China for people arriving in the country.

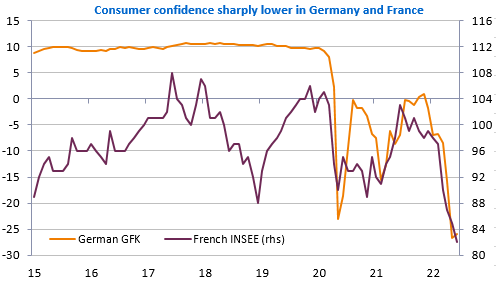

The economic calendar is busy today: household confidence continues to fall in France and Germany, mainly of course as rising prices erode their purchasing power.

These figures will be followed by speeches by ECB central bankers including Mrs Lagarde. Already, the Governor of the Central Bank of Latvia has spoken in favour of a 50bp increase in the ECB’s key rate in July. In the US, a number of important indicators are expected, in particular the Conference Board’s consumer confidence index, but also house prices and the trade balance, whose deficit may have remained above $100bn in May. The US dollar continues to weaken against the euro: 1.06 was even crossed yesterday.

This week’s agenda is very full. You can find it in the Macro and Oil Weekly Report.