WTI-Brent jump

While ICE Brent prompt price for August expiry jumped to 75 $/b on early Tuesday, the spread between US crude (light sweet WTI) and the…

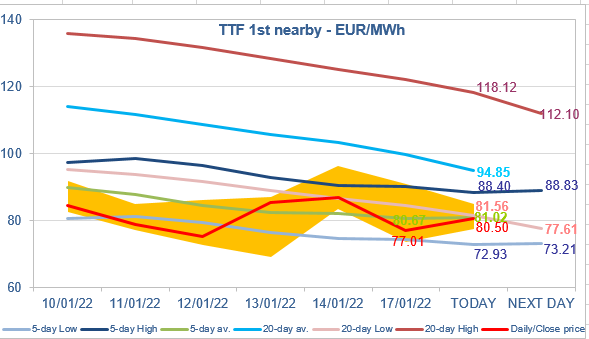

European gas prices dropped strongly yesterday, pressured by weaker Asia JKM prices (-20.88% on the spot, to €66.335/MWh), which implies LNG supply to Europe will remain high. The additional drop in Norwegian supply (to 310 mm cm/day yesterday, compared to 330 mm cm/day on Friday, still impacted by the unplanned outage at the Troll gas field, which has been extended until 20 January) had little impact. Even the prospect of a lasting weakness in Russian flows (Gazprom did not book additional transport capacity via Poland at monthly auctions yesterday and said it will not hold any sales auctions on its electronic platform until 24 January at the earliest) failed to support prices.

At the close, NBP ICE February 2022 prices dropped by 23.780 p/th day-on-day (-11.43%), to 184.3250 p/th. TTF ICE February 2022 prices were down by €9.96 (-11.45%), closing at €77.012/MWh. On the far curve, TTF ICE Cal 2023 prices were down by 90 euro cents (-2.04%), closing at €43.168/MWh.

TTF ICE February 2022 prices have fallen more than we thought yesterday, but they found support around the 5-day Low. They are rebounding this morning, also supported by the additional drop in Norwegian flows (to 292 mm cm/day). The rebound could continue during the session. As a reminder, the “normalization” process requires prices to trade above the 20-day Low.