Key US job report today

No real change on financial markets: equities keep on advancing on optimism about growth, except in Asia where the spread of the variant brings more…

OPEC+ members swiftly decided to ramp up the group’s target production by 400 kb/d, with Saudi Arabia and Russia now required to produce 10.2 mb/d of crude oil in February. In December, Russian crude and condensate production reached 10.9 mb/d, with about 0.8 mb/d deemed to be classified as condensate. With the current production targets, it will be interesting to see if Russian compliance continues to climb, suggesting they hit the upper range of their production capacity. Yet, this month’s OSP for February loading programs will be interesting to see if Saudi Arabia prices its cargos aggressively to commit all of its export programs in the depth of the Chinese refining maintenance season. If so, we could expect a weakening of the Dubai market backwardation.

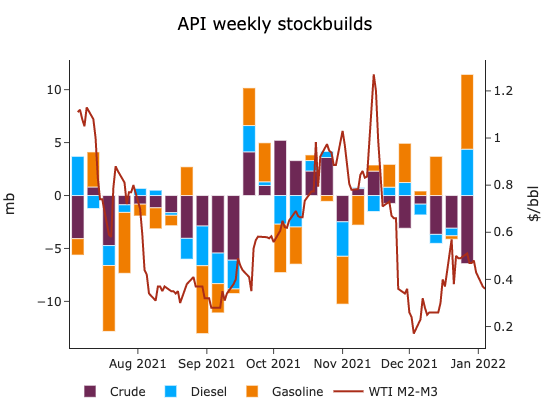

China slashed its refined product export quotas by half in the first allocation of 2022, in an effort to curb domestic emissions ahead of the Olympics. China was a significant exporter of diesel to Asia, averaging almost 400 kb/d in 2019. The current 2022 export program puts refining margins outside China on a stronger footing. Finally, the API survey showed a large build in refined product stocks of about12 mb, combined with a sizable draw in crude stocks of 6.4 mb, potentially catching up with seasonal trends.