First consequences of the war on industrial activity in Europe

The rise in crude oil prices continues. Brent crude is approaching $120/bbl this morning, its highest level in 10 years. A few more $/b and the…

Oil benchmarks continued to drop on Tuesday: ICE Brent front month went -3.3% lower to settle at $102.46/b and NYMEX WTI front month ended the trading session at $99.76/b, -3.2% lower.

Concerns on the state of the economy are growing with Chinese’s lockdowns, the comments of the Fed to further increase interest rates and a stronger dollar. In Europe, Hungary continues to be the main obstacle to obtain unanimous approval of the embargo on Russian oil. As the agreement is delayed oil prices move down.

This morning oil prices erase yesterday loss, ICE Brent quotes +2.3% higher, NYMEX WTI climbs by +2.2% on a decrease of Covid cases in China.

Emirate and Saudi ministers of energy called for an increase in investments in oil projects to face the higher demand for non-Russian oil. Due to underinvestment, spare capacity production is non-existent in OPEC+ countries excluding Saudi Arabia and the UEA. Estimate of EIA found that investment in oil and gas projects fell by 23% following Covid-19 pandemic.

API report on last week inventories shows crude stock increased by 1.6mb, gasoline inventories grew by 823kb and distillates inventories also grew by 662kb.

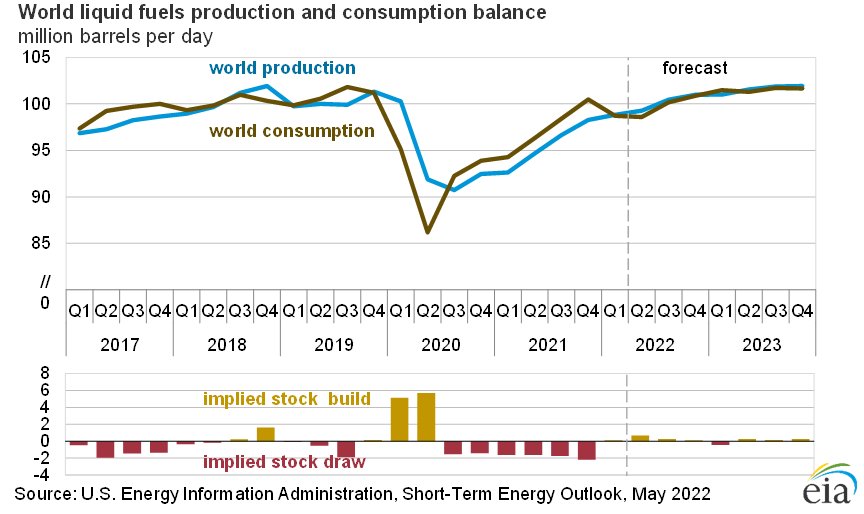

The EIA published its monthly short-term energy outlook: the US administration forecasts average prices will set at $103/b in 22H2 and $97/b in 2023. These prices came from a downward revision of total oil demand of -0.2mb/d at 99.6.6mb/d on average for 2022.