Limited moves on financial markets

Financial markets are rather calm in general, with limited moves on equities, bonds and FX. The EUR/USD exchange rate has edged down but remains not…

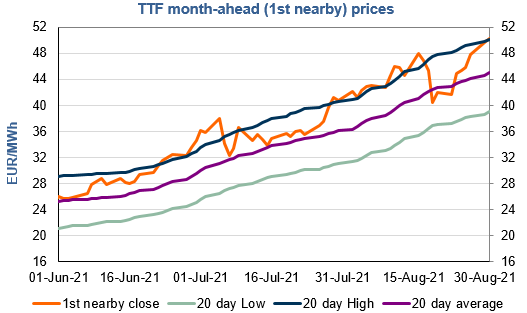

European gas prices rose again yesterday, still supported by relatively weak stock levels and uncertainty over Russian supply for the coming months. The rise in Asia JKM prices (+2.72% for the October 2021 contract, to €52.655/MWh) and in parity prices with coal for power generation (thanks to higher coal prices) provided additional upward pressure.

On the pipeline supply side, Russian flows were stable yesterday, averaging 313 mm cm/day. Norwegian flows were up, averaging 322 mm cm/day (compared to 299 mm cm/day on Monday).

At the close, NBP ICE October 2021 prices increased by 5.100 p/th day-on-day (+4.16%), to 127.710 p/th. TTF ICE October 2021 prices were up by 66 euro cents (+1.33%) at the close, to €50.338/MWh. On the far curve, TTF Cal 2022 prices were up by 21 euro cents (+0.63%), closing at €33.515/MWh, slightly above the coal parity price (€33.148/MWh).

Tight fundamentals could continue to support European gas prices today. However, as prices are now trading at technically overbought levels, profit taking by financial participants and technical resistances (€51.941/MWh on TTF October 2021 and €33.635/MWh on TTF Cal 2022) could contribute to limit gains.