The market remains bullish despite headwinds

The price of Brent 1st-nearby rose above $90/b yesterday even as US crude oil inventories rose for the second week in a row: +2.4mb. But it…

Yesterday, oil prices closed in red territories: ICE Brent front month closed at $118.51/b, making a 2.2% loss while NYMEX WTI for July delivery went 3.0% down to settle at $115.31/b.

The US Fed decision to hike rate by 75bp (see this news) fueled fear for economic growth and thus oil consumption, dragging prices lower. However, oil is still trading at a very high level due to bigger concerns related to supply with the war in Ukraine and a robust demand.

IEA released its monthly report. The organization predicts oil demand should increase by 1.8mb/d in 2022 (unchanged from May report) and published forecast for 2023: a 2.2mb/d increase driven by China. Should these predictions be exact, oil consumption would surpass pre-pandemic level in Q1-2023. The agency found that OPEC+ production was 2.8mb/d behind quotas in May, giving support to oil prices. Commercial inventories were 77mb up in April making the first gain after nearly two years of decline.

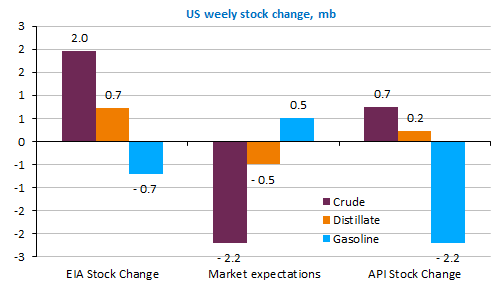

But, If we look at commercial crude inventories, only in the US and only for last week it is also a gain, +2.0mb according to the EIA. Products inventories as a whole were stable: -700kb for gasoline and +700kb/d for fuel oil. US domestic production climbed to 12.0mb/d.

This morning, oil rebounds: NYMEX WTI trades +0.8% higher.