No change for the ECB. US stocks down on prospects of higher tax on capital gains

The ECB meeting had little impact on markets. The reduction in bond purchases was not even discussed Mrs. Lagarde said. The European markets welcomed the…

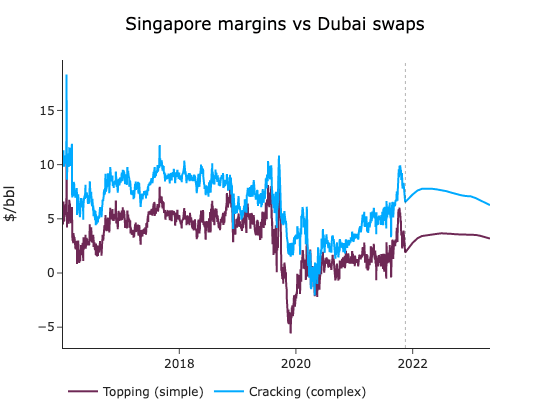

Crude prices continued to hover around the 82 $/b for ICE Brent Jan delivery, amid falling diesel cracks in Europe and the US. Indeed, refining margins have weakened to flip into contango at the prompt for Europe and Asia, as diesel prices softened, fuel oil prices dropped heavily, while gasoline and naphtha remained supported as refiners used an incremental part of the light ends as refinery fuel instead of natural gas. with such low fuel oil prices, refineries are heavily incentivized to run their FCC at maximum rates.

Nigerian officials mentioned that issues that plagued their oil production facilities should be resolved by December. Nigeria had to experience 5 force majeure events since November 2020, symptoms of an ageing oil infrastructure lacking investment. Yet, differentials to Dated Brent have remained subdued all year, indicating that Nigeria also struggled to ship their crude eastward due to the lack of competitiveness against middle-eastern crudes. Nigerian crudes are one of the most valuable crudes on the planet, yielding a high kerosene/gasoil cut, usually above 60% straight out of the distillation tower. In the current market environment, which punishes hydrocracking units, they could resolve the weak margins in the NWE. Yet, European refiners are still below 9 mb/d of crude intake in October, which means that they do not have to source a lot of volume at current rates.