Stable equilibrium

Brent prompt month contract remained range-bound at 55.5 $/b as the dollar remained supported despite a significant unexpected change in the US macroeconomic indicators. Time…

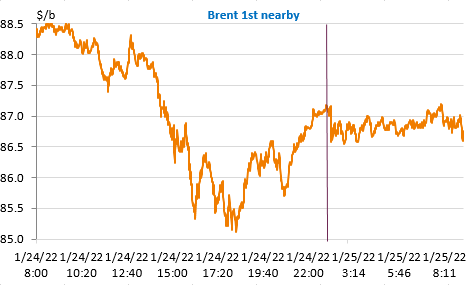

The price of Brent crude oil more or less followed the trend of the equity markets yesterday: initially swept along with all risky assets by a strong sell-off, it fell from nearly $89/b to $85/b before regaining about half of the lost ground, around $87/b. But it cannot be said that rising geopolitical risks in the Middle East and Eastern Europe are creating more volatility in oil prices than in other risky assets, unlike in gas prices.

Prices remain fundamentally supported by the prospects of accelerating demand after the Omicron-related slowdown and the difficulties of supply to adjust. According to Saudi Aramco, demand is on its way back to pre-crisis levels and producers are still not investing enough. But the general context of energy transition is a brake on the resumption of investments. In the United States, the battle is raging: the oil and ethanol lobbies are joining forces to push back the Biden administration’s efforts to equip the federal administration with electric vehicles only. In Japan, the government is subsidising refiners to continue producing gasoline at skyrocketing prices, despite rising production costs. As we reported yesterday, financial investors are positioning themselves massively in favour of higher prices. Many producers seem to be doing the same and no longer hedge their production against a possible drop, convinced that prices will continue to rise