SPECIAL WEBINAR: The storm is raging accros European energy market

EXCLUSIVE WEBINAR Star your free trial & Get access to an exclusive webinar The storm is raging across European energy markets – European gas systems…

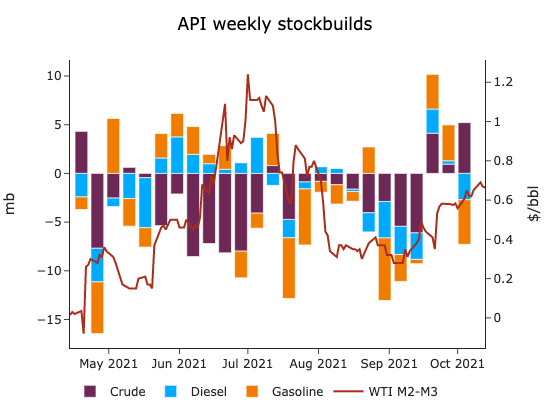

According to the API industry survey, US crude stocks built by 5.2 mb w/w, while Cushing stocks dropped by 2.2 mb, lending support to the greater availability of crude in PADD3 and the Atlantic basin. Indeed, crude stocks are expected to build slightly in the US for the month of October, in line with the refiners’ turnaround season. This partially explains why ICE Brent front-month time spreads continued to weaken throughout the last two weeks, now trading below 65 cents, despite outright prices creeping higher, due to strong inflation hedging pressures, as oil volatility and uncertainty prompted more aggressive hedging programs. On the product side, gasoline stocks are expected to draw by 4.5 mb and distillates by 2.7 mb, pushing lower the total diesel inventories in the Atlantic basin, while the natural gas crisis in Europe effectively reduces diesel supplies due to high hydrocracking costs.