Westerners step up economic and financial pressure on Russia

In the financial markets, last week ended in an almost surreal atmosphere with very strong rises in the equity markets, so much so that the…

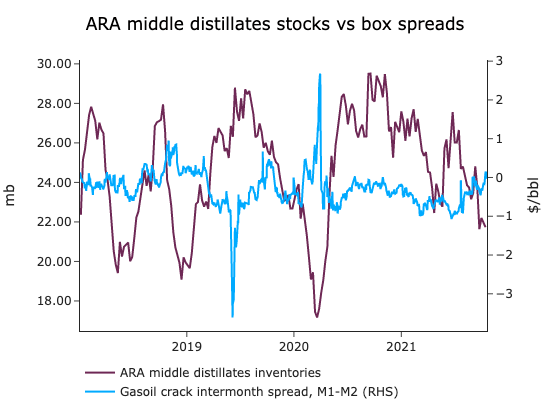

ICE Brent crude futures continued to be supported, at 85.2 $/b for the Dec21 delivery, as stocks data in the US and the ARA region surprised to the downside. Indeed, US stocks were depleted by a combined 11 mb, mainly due to drops in gasoline and diesel stocks, as the US turnaround season took down 1.5 mb/d of refining capacity, leaving the refined product market undersupplied for the time being. In Europe, diesel and gasoline stocks also dipped by 0.3 mb respectively, lending further support to the transportation fuel markets. Jet fuel stocks remained elevated and stable, at 7 mb. Total distillate stocks in ARA (diesel and jet) are approaching the level where we could see a significant increase in the diesel forward curve’s curvature, with the 1st inter-month spread rising much higher than the second inter-month spread. Diesel supply is increasingly problematic in the Atlantic basin, with US refiners’ limited capacity, as Chinese diesel exports remained low in September, and with hydrocracker run cuts in Europe (Total’s Antwerp refinery) and the Middle-east (Fire at a CDU in Kuwait producing ULSD).