Back to reality

The decline in long term bond yields was accentuated yesterday, pulling the US 10 year down to 1.43%, mainly on the idea that Joe Biden might decide to…

Brent 1st nearby is close to $89/b again, a level it exceeded last year. The United Arab Emirates announced that it had intercepted two new missiles fired by Yemeni Houthi rebels. The threat of Russian military intervention in Ukraine also continues to fuel geopolitical risk.

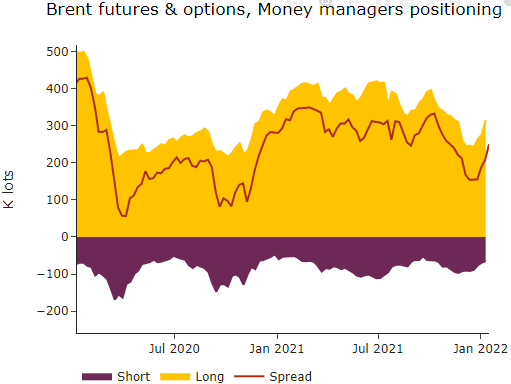

On the demand side, it is confirmed that the Omicron wave has had a more moderate impact than expected and that it is in the process of receding in the advanced countries where air traffic forecasts are improving. In a context still marked by the difficulty of supply to adjust to this rising demand, the level of stocks continues to decline and the market seems to have more and more the key level of the $100/b in sight. Analysts at the major US banks are guiding the market towards this target: Goldman Sachs and Morgan Stanley expect $100/b to be reached in Q3 while Bank of America expects $120/b by mid-year. The latest CFTC figures show that speculative positions are clearly on the rise again (see graph).

It is unlikely that the expected decline in services PMIs in January will have a strong moderating impact on energy prices, especially as industrial PMIs are expected to confirm Omicron’s weak hold on the sector.