Prices weakened in Europe and in Asia

European gas prices weakened overall on Friday, pressured by forecasts of higher LNG supply in Europe in the coming days and profit taking. The drop…

Oil prices went up yesterday: on NYMEX, WTI front month gained less than 0.1%, ending at $105.17/b. On ICE, Brent price was +0.4% up to settle at $107.58/b. Market reversed at the end of the day, as Brent fell as low as $103.10/b during the session.

The main concern was the slowing of the Chinese economy with fears supported by the publication, over the weekend, of PMI figures: factory activity in the country is at the lowest level since February 2020 (when the country faced a first wave of Covid-19). In the US, the factory activity is growing at a slow pace in April, according to the ISM survey (see macro comment). The market was pushed up in the second part of the day due to the rally on diesel futures, whose prices for June delivery jumped by 5%.

More info were released on the incoming embargo of Russian oil in the UE: the sanction package should be finalized today and presented to member states tomorrow, Hungary and Slovakia could benefit an exemption as these countries are highly dependent on oil from Russia, and the embargo should be imposed gradually until the beginning of 2023.

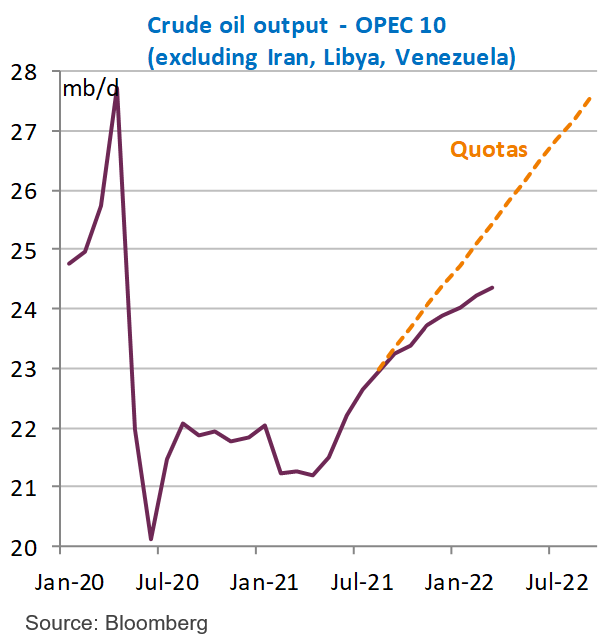

According to Reuters models, in April, OPEC crude output increased by 40kb/d. It is below the 254kb/d target (that is part of a 400kb/d monthly output increased for OPEC+ members), see our Weekly Macro & Oil Report.

This morning oil is trading -0.5% lower, with traders awaiting the publication of the API inventory later today to have a snapshot of crude and products inventories.