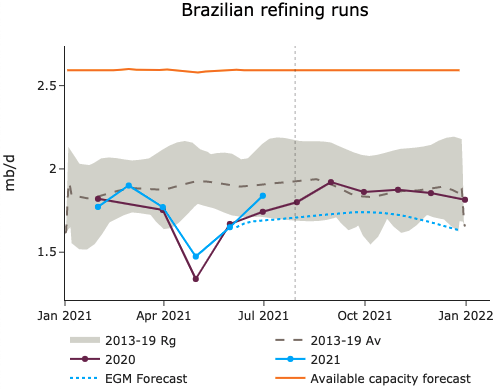

Crude prices continued to rise yesterday, to reach 75 $/b for the ICE Brent August contract on the backend of drawing US petroleum inventories and supportive macro environment for inflation. In their latest EIA data release, commercial crude stocks drew by 4.1 mb, in line with seasonal norms. Gasoline and distillate stocks both declined by respectively 2.3 mb and 3.1 mb, as demand remained elevated across the board. US production was revised down at 11.2 mb/d, more in line with our expectations, as the recent measurement of 11.4 mb/d seemed at odds with the frac spread count and the onshore rig count. The WTI-Brent narrowed shortly after, after reaching a weak 2.7 $/b, to 2.24 $/b. Brazilian runs increased more than expected in June, at 1.7 mb/d, when we expected low utilization rates throughout the year due to the pandemic.

Confidence seems returning a bit on financial markets thanks to good economic indicators and hopes of acceleration in the vaccination campaigns. Bond yields edged up…

Crude oil prices fell back a little overnight, but after rising sharply before a potential Russian attack on Ukraine. The price of Brent 1st-nearby touched…

There is decidedly little happening in the markets this week apart from a fairly sharp rebound in equities, buoyed by strong corporate results, but that…

Join EnergyScan

Get more analysis and data with our Premium subscription

Crude prices continued to rise yesterday, to reach 75 $/b for the ICE Brent August contract on the backend of drawing US petroleum inventories and supportive macro environment for inflation. In their latest EIA data release, commercial crude stocks drew by 4.1 mb, in line with seasonal norms. Gasoline and distillate stocks both declined by respectively 2.3 mb and 3.1 mb, as demand remained elevated across the board. US production was revised down at 11.2 mb/d, more in line with our expectations, as the recent measurement of 11.4 mb/d seemed at odds with the frac spread count and the onshore rig count. The WTI-Brent narrowed shortly after, after reaching a weak 2.7 $/b, to 2.24 $/b. Brazilian runs increased more than expected in June, at 1.7 mb/d, when we expected low utilization rates throughout the year due to the pandemic.