Infographic – EUA prices above €40/t : anatomy of a rally

[UPDATE : 18/03/2021] EUAs are the best performing energy commodity in Europe since the start-up of the COVID19 outbreak. They even reached an absolute record high…

On Wednesday, oil benchmarks slid, ICE Brent for September delivery closed on a 1.2% loss at $112.45/b and WTI front month settled 1.8% lower to $109.78/b.

During the first half of the day, oil gained ground (WTI traded at +2.0% ) but when the Energy Information Administration published its report for two weeks (ending 17 June and 24 June) the market reversed.

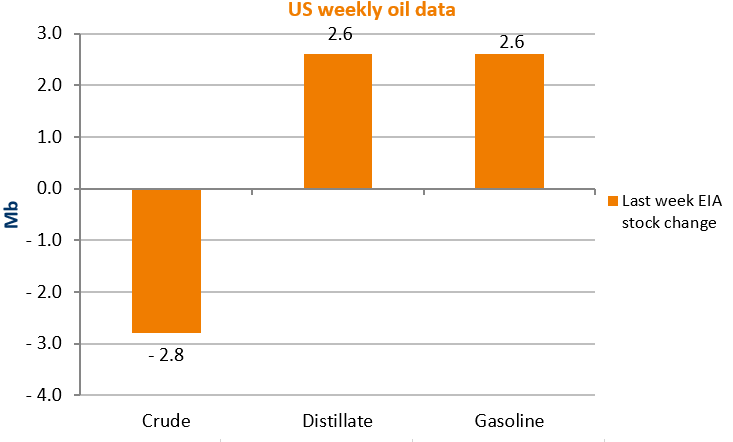

Overall, crude inventories declined by 2.8mb during the most recent week. The bearish factor was the unexpected stock build for gasoline (+1.2% week-of-week) and distillates (+2.3% week-of-week). What is more, US domestic production is ramping up, from 12mb/d three weeks ago to 12.1mb/d last week. The average US gasoline supply (the best proxy for demand) is 600kb/d below the typical level, showing some sign of demand destruction.

Today, OPEC+ ambassadors will decide August production quotas. According to the comments made during the previous meeting, ambassadors would go with a 648kb/d production rise. In fact, the cartel’s members are currently trailing 2.7mb/d behind the required production level. This should be the last production increase of the present agreement, quotas should remain in place until December 2022.

Today, oil is going slightly down, -0.3% for WTI.